-01.png)

CHF WEEKLY ROUND-UP: October 27-31, 2025

- John A

- Oct 31, 2025

- 4 min read

It is Halloween, and markets will be glad to see October behind them, as November and December are historically strong months for equity prices. World markets are looking to recover from a troubling week, with global stock markets mixed-to-firmer and U.S. stock indexes pointed solidly higher.

The TSX looks to be recovering from some wild swings this week, rising on opening. The Venture exchange had an equally rough ride and is inching upward at opening. This morning, Statistics Canada said Real Gross Domestic Product declined 0.3% in August, and early signs suggest the economy barely managed any growth in the third quarter, as goods-producing industries were down for the fifth time this year, while the services side contracted for the first time in six months. On Wednesday, the Bank of Canada (BoC) signalled that it may be finished with rate cuts following its quarter-point reduction, which left the benchmark interest rate at 2.25%. BoC Governor Tiff Macklem said it would take a material change in the economy compared to the central bank’s forecasts to warrant further easing. Prime Minister Mark Carney suggested Canada’s relationship with China is at a “turning point” following his meeting with Chinese President Xi Jinping, on the sidelines of the Asia Pacific Economic Cooperation Summit (APEC) in South Korea. They discussed solutions to respective sensitivities regarding issues including agriculture and agri-food products such as canola, as well as seafood and electric vehicles. It’s been eight years since a Canadian prime minister has met with the president of China.

U.S. markets made new all-time highs again this week, and year-end targets have been raised again. On Wednesday, as widely expected, the U.S. Federal Reserve trimmed its benchmark funds rate to a range of 3.75% to 4.00%. Fed Chair Jerome Powell held back on committing to further rate reductions as the labour market cools and inflation persists. The ongoing government shutdown means the Fed is missing key data, inflation remains stubbornly high, and the labour market is showing signs of cooling, pointing to a level of uncertainty the Fed dislikes. The U.S. dollar (USD) has been strongly rising through October to a level not seen since mid-May. President Trump made trade deals with four Southeast Asian countries at the APEC and assured leaders they can look to the U.S. for its full support and friendship for years to come. A meeting between President Trump and Chinese Leader Xi Jinping in South Korea on Thursday ended in a truce. The U.S. pulled back from sharp tariff increases, lowering the duty on China to 47%. China agreed to resume purchases of U.S. agricultural products, including soybeans, and to extend a one-year pause on the export of rare earth elements.

Some level of consolidation at the USD$4,100.00/oz level is seen in gold, following the recent high level of price volatility. Spot gold is at USD$4,015.70/oz this morning. Silver prices are consolidating at USD$48.87/oz today. The seasonal trend for precious metals is strong into the spring, and this should reassert itself going forward. Gold is the safest money, and the underlying reasons to hold gold remain, as major buyers continue to be active and buying during the recent price dips.

Copper is trading above USD$5.00/lb this morning and has been in a general uptrend since mid-2022, beaten up by the recent tariff nonsense but starting to assert itself. There may be a short-term price challenge in the next month, but that will be a buying opportunity. Other than nickel, the other base and industrial metals have been showing price gains throughout the last month. Any degree of trade cooperation with China may put limited stability into metals trading.

Cobalt prices are up almost 40% in the last two weeks; however, exports from the Democratic Republic of Congo (DRC) are set to resume next month and will determine how far the current price rally could go. Lithium prices are up over 11% in the last two weeks but remain near two-year lows. The waiting game in battery materials continues. Look for opportunities among issuers with high-quality projects and the ability to sustain through the duration of price weakness.

Rare Earth Elements (REE) have been a hot topic lately, and an agreement between the U.S. and China on export restrictions may bring some short-term stability. This agreement has negatively impacted the valuations of REE issuers. China remains a poor partner, and REE demand will grow; projects with development potential will become important as processing capability develops outside China. Canada has great potential in this area, and “Nation-Building" projects should focus on this sector. Uranium prices rebounded 6.5% in the last two weeks after positive announcements on nuclear power development in Ontario and the U.S. were made.

We are pleased to present our round-up of client news released between October 27 and 31, 2025.

Mining

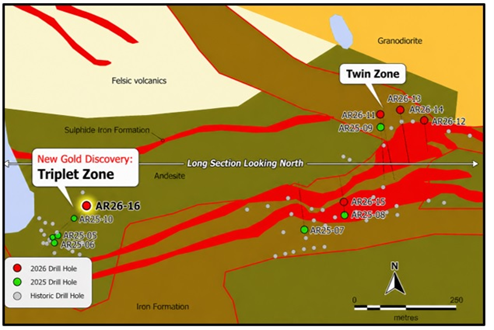

On October 31, 2025, Sokoman Minerals Corp. (TSXV: SIC) (OTCQB: SICNF) announced that it had closed its “bought-deal” private-placement offering for aggregate gross proceeds to the Company of $26,221,750. The net proceeds from the sale of the Common Shares will be used by the Company for property acquisitions as well as working capital and general corporate purposes. The gross proceeds from the sale of the FT Shares will be used to incur Canadian exploration expenses.

The offering consisted of:

53,000,000 common shares of the Company (the "Common Shares") at a price of $0.19 per Common Share for aggregate gross proceeds of $10,070,000; and

60,950,000 common shares of the Company (the "FT Shares") that will qualify as "flow-through shares" including 7,950,000 FT Shares issued pursuant to the full exercise of the over-allotment option, at a price of $0.265 per FT Share for aggregate gross proceeds of $16,151,750. The FT Shares were distributed on a charity flow-through basis.

Mr. Eric Sprott, through 2176423 Ontario Ltd., a corporation beneficially owned by him, acquired 53,000,000 Common Shares in connection with the Offering.

SAVE THE DATE

Our CHF clients — Sokoman Minerals Corp. (Booth #57) and Rocky Shore Gold (Booth #16) — will be attending the Mineral Resources Review 2025, taking place November 4–7 in St. John’s, NL.

Register here to attend.

Comments