-01.png)

CHF WEEKLY ROUND-UP: Feb. 2 - 6, 2026

- John A

- Feb 6

- 9 min read

World shares were mixed after Wall Street extended losses driven by heavy selling of technology stocks. Confusion about who Kevin Warsh, President Trump’s pick for the next Federal Reserve (Fed) chair, really is and what he stands for continues. It has been assumed that Warsh is a sort of "inflation hawk" and will raise interest rates. Warsh believes that the U.S. is undergoing a productivity-led growth boom and that fiscal policy’s role is to spur economic activity by keeping taxes low and regulations light, while monetary policy’s role is to spur investment by keeping interest rates low. He supports Fed policymaking that is less reactive to the latest economic data. Technology stocks continue to underperform because intensifying competition in the AI space is forcing tech giants to compete more with one another and significantly increase their AI infrastructure spending, creating uncertainty about future earnings growth. Materials prices have come under pressure for reasons unrelated to metal price drivers. One week of erratic trading is not a top; bubbles are not bursting, nor is there a reason to sell everything. We have not seen the kind of irrational exuberance that marks the end of a bull market. The Bull/Bear ratio has become overextended and is working its way back to balance. Be invested in quality, watch the fundamentals.

The European Central Bank left its benchmark deposit rate unchanged at 2.0% on Thursday, as the EU economy showed inflation just below 2.0% with modest yet resilient growth, supported by low unemployment and increased government spending on defence and infrastructure. Euro Markets were positive on this move. Inflation in the UK has risen to 3.4%, prompting the Bank of England (BoE) to freeze its benchmark Bank Rate at 3.75%.

The TSX experienced two sharp drops this week from its all-time high the previous week, but it is down less than 2.0% and down less than 1.0% in the last month, but popped up this morning. The Venture exchange is down almost 10% in the last week after hitting a ten-year high the previous week, but jumped 3.0% at opening today. There is a lot of opportunity in the resource-heavy Canadian markets as metal prices are being hit by speculators. Statistics Canada reported that the economy shed 25,000 jobs, largely coming from the private sector and part-time work, in the first month of the year, but a drop in the number of people looking for work drove the unemployment rate down to 6.5%. The Canadian economy is struggling despite Bank of Canada interest rate cuts; per capita GDP is still falling, and growth is only 1.0% annually. Major projects and accelerated homebuilding have yet to materialize, and trade uncertainty persists.

On Tuesday, President Trump signed a bill ending a partial shutdown of most of the government since Saturday morning. The House narrowly passed the bill after the Senate approved it last week. The bill provides funding through the remainder of the fiscal year to September 30. The S&P 500 slipped about 2.0% this week and posted its sixth decline in seven days. Despite the index being dragged down by the overweight of the big tech names, most of the other stocks in the S&P 500 advanced as the market breadth increased. No rate cut by the Fed is expected through the June 17, 2026 meeting, the first one with Kevin Warsh as Fed chair, if the Senate confirms his appointment. Some are calling for a March rate cut, but Chair Powell will likely just ride his term out. U.S. inflation appears to be moderating to the Fed’s target of 2.0% y/y, but it could remain sticky around 3.0% for a while. The value of the U.S. dollar (USD) had been increasing against world currencies since Warsh was named, but seems to be settling back into range today. Maybe the dust is settling. The rally in the U.S. dollar index during the past couple of weeks has reduced bullish enthusiasm in gold and silver.

Gold and silver prices have been volatile again this week following a months-long rally as investors moved into safe-haven assets, prompted by factors including elevated geopolitical tensions. Spot Gold prices are modestly higher at USD$4,930.40/oz in early trading today. Silver opened at USD$76.02/oz today, posting solid losses this month, and hit a seven-week low below USD$70.00/oz overnight. Silver demand has not declined, and supply remains in deficit. Platinum and Palladium prices are recovering as well. Commodity analysts at CIBC now see the market averaging USD$6,000.00/oz, and silver prices averaging around USD$105.00/oz this year. Always remember, Gold is the constant; the dollar is the variable. New World Orders and Reserve currency shifts take decades to be completed. Currently, the precious metal stocks are not reflecting this reality, and many investors are still clinging to technology shares, ignoring the emerging opportunities in precious metals stocks. Gold producers are highly profitable, and prices do not truly reflect this yet. Issuers with resources in the ground will be re-rated; explorers have been raising cash, and discoveries will follow. Be invested in this sector.

Base and industrial metals are all on the rebound today, with Copper at USD$9.94/lb and rising. Nickel at USD$7.66 is still down 10% from recent highs. The world is still drastically short of these resources, and new mine production is a long process. Opportunities in the junior space abound.

Cobalt price has held steady at USD$25.53/lb, and Lithium price is down to USD$20.75/kg, still more than a two-year high. Prices for Lithium and rare-earth battery and motor compounds are rising in China.

The Trump administration announced on Wednesday that it intends to create a critical minerals trading bloc with its allies and partners, using tariffs to maintain minimum prices and counter China’s dominance over the key elements needed for everything from fighter jets to smartphones. “Project Vault,” a plan for a strategic U.S. stockpile of rare earth elements to be funded with a USD$10 billion loan from the U.S. Export-Import Bank and USD$1.67 billion in private capital. The European Union and Japan, together with Mexico, announced agreements to work with the United States to develop coordinated trade policies and price floors to support the development of a critical minerals supply chain outside of China. The countries said they would develop an agreement about what steps they will take and explore ways to expand the effort to include additional like-minded nations. The Canadian Foreign Affairs Minister was in Washington on Wednesday attending the meeting, but no word on participation was forthcoming. This underscores the need to finalize the U.S.-Mexico-Canada trade agreement and strengthen North American solidarity.

We are pleased to present our round-up of client news released between February 2 and 6, 2026.

Mining

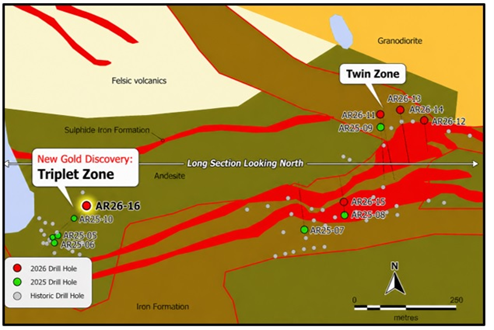

On February 2, 2026, Arya Resources Ltd. (TSXV: RBZ) reported weighted average gold (Au) and silver (Ag) assay results for drill holes AR25-007, AR25-008 and AR25-009 completed at the Twin Zone of its Wedge Lake Gold Project in Saskatchewan's La Ronge Gold Belt. Silver assay results from the Company's 2025 drilling program have now been integrated into the previously reported results, confirming the presence of consistent silver credits associated with gold mineralization.

"Today's averaged gold-silver assay results suggest that the Twin Zone gold system at Wedge Lake is robust over long drill intervals, with a gold signature and a silver credit that adds value to the overall mineralization picture," said Rasool Mohammad, President & CEO of Arya Resources.

On February 2, 2026, Libra Energy Materials Inc. (CSE: LIBR) (OTCQB: LIBRF) (FSE: W0R0) announced mobilization for a drilling program at its 100%-owned Stimson Project, located within the Case Lake Lithium-Cesium District in Ontario. Stimson represents Libra's newest acquisition within its Ontario portfolio, after the Company acquired a 100% interest in the Project.

"We are ready to kick-off the new year with our first-ever drill program at Stimson. The initial scout hole will test a historical unsampled hole which returned at least three intervals of possible spodumene, located proximal to the same geological sub-province boundary that hosts Power Metals' nearby Case Lake lithium-cesium project (one of the largest cesium resources globally). With excellent infrastructure and access, we expect the drill program to be a cost-effective way to quickly evaluate whether further work would be warranted at Stimson. We would like to thank the Apitipi Anicinapek Nation representatives for their support in making this drill program possible," said Koby Kushner, Chief Executive Officer of Libra.

Regional map, showing geology, nearby claims, and infrastructure.

Stimson is strategically located along strike of Power Metals' Case Lake lithium-cesium deposit, straddling the same boundary between the Quetico and Abitibi sub-provinces. Importantly, a historical drill log at Stimson noted three intervals in DDH PT94-11, the largest being 39.8 metres (60.0 m – 99.8 m) logged as a 'granitic complex', an unknown portion of which was pegmatite containing possible spodumene (OGS Assessment Record 42H02SE0010). This historical result provides evidence of a potential lithium-bearing pegmatite system on the Project that Libra plans to assess through its initial drilling campaign. Although Libra is primarily targeting spodumene, the key lithium-bearing mineral found in lithium-cesium-tantalum ("LCT") pegmatites, the Company will also evaluate the potential for pollucite, which is the main cesium-bearing mineral in LCT pegmatites.

On February 3, 2026,

Arya Resources Ltd. (TSXV: RBZ) announced that a new round of drilling at its Wedge Lake Gold Project in Saskatchewan had commenced. This drilling will focus on two key areas of the project: the Twin Zone and the T-6 Zone, where earlier drilling returned encouraging gold results.

Arya has identified two distinct styles of gold mineralization at Wedge Lake:

T-6 Zone: Orogenic / Mesothermal gold mineralization

Twin Zone: Iron Formation-hosted gold mineralization

On February 5, 2026, Athena Gold Corporation (CSE: ATHA) (OTCQB: AHNRF) provided an exploration update from its Excelsior Springs Project in Nevada and its Laird Lake Project in Ontario.

Mammoth Minerals Limited (ASX: M79) has been aggressively exploring Excelsior, to earn an 80% interest in the project over five years, providing Athena a free-carry to Definitive Feasibility Study. Recently, Mammoth reported significant announcements from its ongoing exploration campaign. See Mammoth News here.

A ~5,000m, eight-hole, diamond drilling program has been designed at Laird Lake, located in Ontario's world-class Red Lake Gold Camp. The drill program will leverage historical SkyTEM magnetic and electromagnetic data, which has been reprocessed to further refine targets prior to drilling, further details of which the Company plans to release in the near term. The Company applied for drill permits in September 2025 and completed a Species at Risk Mitigation Plan in December 2025. While the Company continues to experience ongoing delays in the permitting process, it remains actively engaged with relevant stakeholders and regulatory authorities and is fully committed to advancing the project. It is optimistic that permits will be delivered shortly, enabling drilling to commence within the quarter.

On February 5, 2026, Pirate Gold Corp (TSXV: YARR) (OTCQB: SICNF) released episode 4 of the Treasure Hunters video series. In this episode, the crew takes fresh drill core from the depths to the shack, logging structures, splitting core, scanning for gold, and locking in assays with strict QA/QC as they chase the mineralization.

Pirate Gold’s Executive Chair & CEO, Denis Laviolette, presented at the recent VRIC conference in Vancouver on charting the course for the district-scale orogenic gold hunt in Newfoundland.

Fintech

On February 3, 2026, Tenet Fintech Group Inc. (CSE: PKK) (OTC Pink: PKKFF) provided an update regarding the failure to file a cease trade order (the "FFCTO") issued on the Company's securities by the Ontario Securities Commission (the "OSC") on May 7, 2025. While the Company continues to work with the OSC with regard to the ongoing disclosure record review, there is no definitive timetable for the completion of this process and a revocation of the FFCTO, is issued as a result of the Company's delay in filing its annual financial statements, management's discussion and analysis (MD&A) and related officer certifications for the year ended December 31, 2024.

The required documents were filed on October 1, 2025, and Tenet had applied for full revocation of the FFCTO to the OSC on October 6, 2025. As part of the review process, Tenet has agreed to refile certain past MD&As, deemed to be deficient in their disclosures, and anticipates such filings will occur at the end of the review process. Questions have also been raised, including but not limited to revenue recognition and expected credit loss provisions, which may also require the restatement of some recently filed financial statements covering the same periods as the MD&As.

While the review process for the Full Revocation Application continues, the Company has applied to the OSC for a partial revocation of the FFCTO to permit a private placement financing that would allow Tenet to maintain its operations and cover essential expenses.

The proposed private placement financing would consist of the sale of up to 52M common shares of the Company at a price of $0.05 per share for gross proceeds of up to $2.6 million. There can be no assurances that the Partial Revocation Application will be approved by the OSC or that the Private Placement will be completed on the terms set out herein, or at all. The Company plans to issue a news release if/when the Full Revocation has been approved, after which the Company intends to apply for reinstatement of trading of its securities on the CSE.

Comments