-01.png)

CHF WEEKLY ROUND-UP: April 20 - 24, 2026

- John A

- Apr 24

- 3 min read

No settlement of the War occurred this week, and global shares were also unsettled, mostly lower as oil prices rose. Talks between the U.S. and Iran on ending the war are stalled, and while the ceasefire gets extended indefinitely, no overall peace agreement appears to be forthcoming. Who currently represents the Government of Iran is unclear at this point, so who exactly is the United States negotiating with? The Iranian military appears determined to keep the war going. Apparently, the Speaker of the Iranian Parliament and Tehran's lead negotiator has resigned from the negotiating team due to excessive interference from the hardliners in the Islamic Revolutionary Guard Corps. When Xi meets Trump on May 15th, something may shift. Given the extent of damage to energy infrastructure in countries around the Arabian Gulf, even a full reopening of the Strait of Hormuz would fall far short of restoring normal oil flows. The resulting supply shock is likely to last longer than many expect. Energy assets, therefore, remain a buying opportunity.

The TSX composite index appeared to be climbing back to its all-time high last week, but slid back this week, losing 1% of its value. The Venture exchange was down 3.5% this week amid uncertainty in oil and gold prices. On Monday, Statistics Canada said Canada’s inflation rate rose to 2.4% in March, up from 1.8% in February, due to a record surge in fuel costs. The Bank of Canada (BoC) is not planning to adjust interest rates now, as it could be premature and hit the economy even harder. Next Wednesday’s rate announcement is likely a hold.

Losses in U.S. markets were broad-based, with every sector in the S&P 500 finishing lower except Energy. Commodities were choppy, as WTI crude swung sharply. Kevin Warsh, still the probable next Federal Reserve (Fed) chair, wants to lower the federal funds rate sooner, even though few Fed members agree with him. Do not expect any rate moves at next week’s announcement. The U.S. dollar gained this week but is down today. A falling U.S. dollar is inflationary, and that works against a rate-cutting policy. Gold should perform well under that eventuality.

Gold starts today at US$4,706.00/oz and silver at US$75.81/oz. Precious metals were under pressure this week as unnerved investors, overreacting to short-term uncertainty and volatility, extracted cash and moved into treasuries, even though gold is the ultimate safe haven. This created another buying opportunity for China’s central bank, which viewed the recent price declines as attractive and, in March, purchased more gold than in any single month in over a year. Chinese silver imports rose to 836 tonnes in March, the highest ever. Looking past the present conflict to the medium term, gold and silver prices should continue to rise. Do not get distracted by the war headlines of the past month. Hold on to your gold and buy precious metal shares on the dips. Mid-sized producers look cheap, and major companies seem ready to pay to acquire attractive projects.

Copper continues to hang in just below the important US$6.00/lb mark, at US$5.97/lb this morning and 38% higher year-over-year during the first quarter of this year. Nickel is showing a bit of strength at US$8.36/lb today, the highest this year. Owning issuers with copper resources, both new and existing projects, should be considered an investment priority.

Lithium prices surged past US$25.00/kg to US$25.32 in the last 10 days, while Cobalt held at US$25.53/lb. Prices for battery-ready chemicals have been rising over the past month. Uncertainty over oil prices and supply has seen a resurgence of interest in battery EVs and energy storage systems. The drive for critical and technology materials outside of China’s production control continues, especially for rare earths. Increasing interest in nuclear power has caused Uranium prices to rise for the past month.

We are pleased to present our round-up of client news from April 20 to 24, 2026.

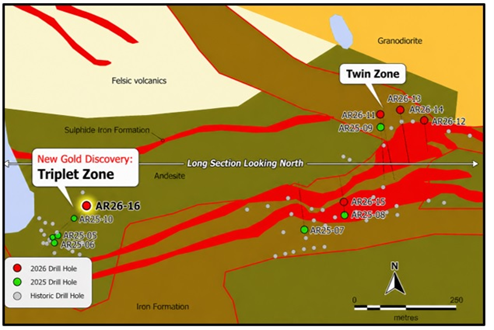

Mining On April 21, 2026, Athena Gold Corporation (CSE: ATHA) (OTCQB: AHNRD) provided an exploration update from the ongoing drilling campaign at its flagship Laird Lake project, in Ontario's world-class Red Lake Gold District. The fully-funded diamond-drilling program commenced earlier this month, with the first hole targeting the G1 geophysical anomaly on the western portion of the project. The hole was successfully drilled to its target depth of 336 m, intersecting broad zones of prospective sulfide mineralization.

Koby Kushner, CEO of Athena said "Encouraging visual results this early in our drilling program at Laird are incredibly exciting. The presence of sulfide minerals within banded iron formation, at the heart of the G1 anomaly, is the right step towards a new discovery in Red Lake, Additional results from other never-before-tested targets are eagerly anticipated. To accelerate the next phase of exploration, the initial rig is being replaced with a larger drill at Laird Lake, allowing for a more aggressive test of deeper geophysical anomalies."

Comments