-01.png)

CHF WEEKLY ROUND-UP: September 30 - October 4, 2024

- John A

- Oct 4, 2024

- 4 min read

October is often the month for surprises. Faced with a very uncertain election, a sea of international risks, international wars, and struggling global economies, anything could happen to sink the markets or just as easily drive them to new heights. Today, the S&P 500, DJIA, NASDAQ, and TSX remain at or near their record highs. This week, the U.S. dollar has bottomed and moved up on positive economic news. The danger is that inflation may re-accelerate.

Growth in Canada remains muted, and The Bank of Canada (BOC) will likely continue cutting its key policy rate by 25 basis points at the October 23 rate announcement. BOC has moved from a plan based on slowing the economy as Canadian Inflation is now in their target range. Greater emphasis is needed on growth and preventing a damaging recession. Economic growth is still expected to pick up next year but may require that the BOC cut its key interest rate below three percent sooner.

The S&P/TSX Composite Index opened at a new all-time high of 24,114 Today. Analysts suggest that Canada trades at a massive valuation discount relative to the US. The best risk-adjusted trade is to avoid China, buy commodities, and buy Canada.

The U.S. economy continues to expand, employment statistics were surprised by the upside this morning, and the U.S. dollar strengthened. Unemployment dropped from 4.2% to 4.1%; yields are up, and the 10-year is getting close to 4%. Markets are up across the board. Another rate cut of 0.25% is expected this year from a Fed still behind the market. Chances of a “Soft Landing” are questioned. U.S. stocks are trying to make new highs as analysts forecast rising earnings growth, and they are expecting a year-end rally to over 5,800 on the S&P 500 index, which may already be underway.

Gold felt some pressure on the release of U.S. job numbers but recovered to USD$2,651 this morning. There is room for gold prices to continue rising through the end of the year to a target of USD$3,000/oz in Q1 2025. Buying opportunities will appear in gold and gold equities, especially in the undervalued junior sector, where discoveries are made. Silver opens at $USD31.78/oz today, as it looks to catch up with gold as the preferred investment metal.

Base metals were positive through September but are being hit by the strength of the U.S. dollar this week. Copper is near USD$4.44/lb today. Nickel has been climbing for three weeks and is near USD8.01/lb this morning. Other metals are following the same trend. Uranium continues to find support at USD$82.15 this week.

Uncertainty over recovery in China also impacts battery and critical material markets. Lithium started to move up in the last three weeks, and while the price is still meager, at USD$10.75 /kg, it may be time to reconsider the Lithium juniors. Cobalt is showing no movement at USD$11.00. China’s economic stimulus is intended to drive its manufacturing sector and maintain its dominance in EVs and critical metals. Supply shortages for EV materials are showing up. Positive actions are being taken to develop the U.S. and Canadian supply chains and ensure domestic security, which will be suitable for driving the energy transition. It is undoubtedly an excellent time to look to Western supply chain players for significant growth opportunities.

It has been a productive week for our clients, and we are pleased to present our round-up of their news released between September 30 - October 4, 2024.

Mining

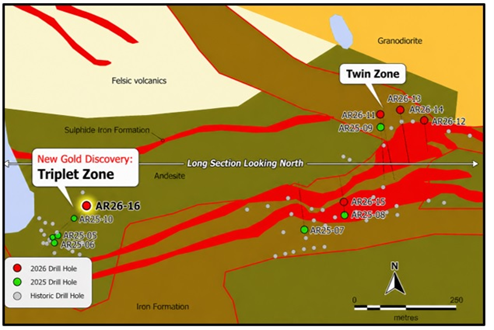

On October 3, 2024, Sokoman Minerals Corp. (TSXV: SIC) (OTCQB: SICNF) provided an update on the drilling program at the 100%-owned Fleur de Lys Property located in the Baie Verte Mining District of northwestern Newfoundland. To date, 1,442 metres of NQ-sized diamond core drilling has been completed in 16 holes. No assays have yet been received from the 465 core samples sent to Eastern Analytical Ltd. in Springdale, Newfoundland.

The 2,000 m Phase 1 program is assessing two historical, as well as new targets generated by Sokoman’s 2021-2024 till and prospecting programs that include the Golden Bull Prospect (boulder field) discovered late in 2023. Drilling is focussing on an approximately 8 km2 area that includes several discrete targets highlighted by the Golden Bull Prospect area. Drilling has tested six separate targets (see Map 1). Other targets located several kilometres further north will be tested in the coming weeks.

Holes FDL-24-01 to FDL-24-04 tested quartz breccia zones 2 km southwest of the Golden Bull Prospect target area and that gave anomalous gold values up to 2 g/t Au from random rock grab (outcrop and float) samples in 2022 and 2023. No previous drilling tested the zones. All four holes intersected sheared / locally brecciated psammitic schists with variable quartz veining and 1%-2% disseminated pyrite over core lengths of 0.5 m to 4.0 m.Drill holes FDL-24-05 to FDL-24-08 tested geophysical / soil geochemical targets underlain by a strong north-trending structural corridor, originally defined by Noranda in 1988 but never tested. Two of the holes (FDL-24-07 and 08) intersected quartz veining with variable sulphide (1%-3% disseminated pyrite and pyrrhotite) over 2.9 m to 10.0 m core length.

CEO Tim Froude, P.Geo., appeared with mining analyst Allan Barry Laboucan on his “Rocks and Stocks News Show” to discuss the Company's Fleur de Lys Gold Project, Phase 1 diamond drilling program updates.

Congratulations to the Porcupine Prospectors and Developers Association and Ontario Prospectors Association for the well organized and informative Northeastern Ontario Mines and Minerals Symposium held in Timmins, Ontario this week. Ontario Regional Geologists reported on progress in the 3 mining divisions in northeastern Ontario where the number of projects and the capital expenditure increased substantially year over year. Presentations by several exploration companies highlighted discoveries and developments of mineral commodities.

Many of these regional events are held in the Fall and are a great source of information on mining activities and can help choose investment targets.

Comments