-01.png)

CHF WEEKLY ROUND-UP: June 23-27, 2025

- John A

- Jun 28, 2025

- 5 min read

What a difference a week makes! Global markets had a positive week. Geopolitical tensions have eased considerably following a ceasefire between Israel and Iran, even as both sides had to get the last shot in. Trade deals appear to be happening, as a U.S.-China agreement on how to expedite rare earth shipments to the U.S. was announced, India may be close, and up to ten other deals appear imminent. The original 90-day pause, with the July 9 deadline for reaching new trade deals, may be extended for countries where "the deadline is not critical”. President Trump retains the authority to impose or adjust reciprocal tariffs based on what he deems beneficial for the U.S. and its workers.

The TSX was lower at opening today, as weaker gold and oil prices drove selling, but has started moving back up. The TSXV has gained 3.5% this month as investors continued to be attracted to junior issuers. Tuesday, Statistics Canada reported that the annual pace of inflation remained steady at 1.7 percent in May. Economists had broadly expected inflation to remain unchanged and that the trade war would likely keep the economy soft in the months ahead. Core inflation was moving in the right direction last month, but not enough on its own to convince the Bank of Canada (BoC) to cut rates again following two consecutive rate holds in recent decisions. The central bank will get the June inflation figures before its next rate announcement on July 30, 2025. Statistics Canada reported that GDP was down 0.1 percent in April as the manufacturing sector slowed, but also said its early estimate for May points to another 0.1 percent decline. The outlook is heavily dependent on how Canada-U.S. trade negotiations evolve, but expectations are that a trade deal will arrive within a month. The soft economic backdrop should give the BoC space to deliver two more 0.25% cuts this year. A forecast published by Deloitte Canada, on Wednesday, calls for a modest recession to hit later in the year as uncertainty and weakness caused by tariffs start to bite into consumer confidence.

Any day with a ceasefire holding in the Middle East is a good day for stocks. U.S. stock futures were pointed up this morning with new all-time highs for the S&P 500 within reach. The technology-heavy Nasdaq also closed at an all-time high Thursday, as U.S. equities rallied through the week. Federal Reserve Chair Powell reiterated that tariff-driven inflation is too uncertain for an immediate cut, but the door remains open if labour or price data soften. The Fed is waiting to see incoming data for June, July, and August before feeling more confident that it can move on rates in September. The U.S. dollar (USD) fell to a 3.5-year low.

Gold, opening at USD$3,260/oz today, is showing little reaction to today’s announcement of a 2.7% annual rise in U.S. consumer prices and slowing growth, as its geopolitical safe-haven appeal continues to diminish. Gold has fallen to the midpoint of its trading range in the last two months since its all-time high, still above the support at the USD$3,250/oz mark. Other precious metals: silver at USD$35.90/oz and platinum at USD$1,330/oz are also under pressure today. M&A action in the sector continues as Torex Gold has launched a takeover for Reyna Silver via an all-cash deal valued at $36 million gaining access to projects in Nevada and Mexico. Torex has also agreed to a financing arrangement, purchasing units of Reyna Silver for a total of $1.1 million.

Base and industrial metal prices were positive throughout the week as trade concerns began to fall away, looking towards clarity on U.S trade policy. Copper is at USD $5.02/lb. today but was over the $ 5.05/lb. mark early in the week with the last global rush to ship copper to the U.S. putting a strain on supply. Glencore has declared its Mount Isa copper smelter unviable and is awaiting a response from Australia’s federal and Queensland’s governments regarding requests for financial assistance to keep the facility running. Glencore cited unprecedented smelting market conditions, including high energy, gas and labour costs, and a shortage of copper concentrates due to Chinese competition for smelter feed. Teck Resources has secured an environmental assessment certificate to extend the life of its Highland Valley Copper mine in British Columbia, keeping Canada’s largest copper operation running into the mid-2040s.

Battery, critical and electric, materials continue to struggle with slower than expected demand growth from the electric vehicle industry provides little prospect for a return to the boom years. The world’s second-biggest lithium miner SQM is laying off 5% of its Chilean workforce as battery lithium prices fell to $8,450 a tonne in June from above $80,000 in November 2022. In China, government support keeps loss-making mines on life support. In more positive developments Energy Fuels received final regulatory clearance to develop the Donald rare earth elements (REE) and mineral sand project in southeast Australia. Look for additional developments in REE supply outside of China for opportunities. While Critical materials were on top of the agenda at last week’s G7 a serious disconnect remains between the Net-Zero vision of political leaders and the practical realities of the global mining industry.

Ending a policy in place since 2013, the World Bank has lifted its ban on funding nuclear energy projects, citing rising global electricity demand and the need for low-emission technologies. Uranium reached USD $ 78.50/lb, this week. The government of Niger announced its intention to nationalize the Somair uranium joint venture operated by French nuclear fuels company Orano, that has been shut out of the mine since December 2024, when the military seized control of the operation.

More in what is becoming a troubling trend, Burkina Faso has completed the transfer of five gold mining assets to the country’s state-owned miner on Wednesday, finalizing a process that began in August to increase control over its mineral resources. Mali plans to restart operations at Barrick Mining’s Loulo‑Gounkoto gold complex under a court-appointed temporary administrator after seizing control earlier this month. Country risk is a major concern for investors in materials sectors.

We present our round-up of client news released between June 23-27, 2025.

Mining

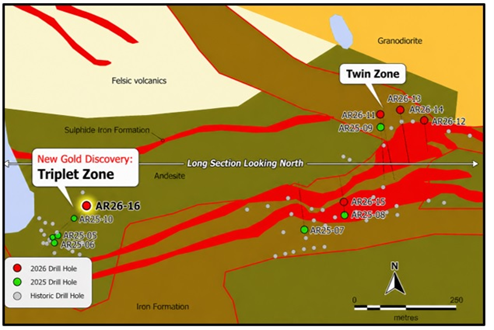

On June 24, 2025, Rocky Shore Gold Ltd. (CSE: RSG) announced that a fully permitted summer exploration program has begun at its 100%-owned Gold Anchor Project in central Newfoundland, Canada. The program will focus on its recently discovered 6,000-metre-long Lane Pond Gold Target, which is strategically located along the prolific, gold-bearing Appleton Fault. The Appleton Fault is a major gold-bearing fault zone trending for greater than 150 kilometres in central Newfoundland and hosts significant untested gold targets, diamond drill discoveries and a gold resource on the adjoining property located northeast of Gold Anchor.

Ken Lapierre, President and Chief Executive Officer, commented, “We are delighted to kick-start the summer field season at Gold Anchor. The program will include detailed till sampling, prospecting, geological and geophysical work at its Lane Pond Gold Target and other high-priority gold targets in the vicinity. At Lane Pond, significant gold values have been found in recent and historical sampling in an area 6,000 metres long and located proximal to the Appleton Fault. The Appleton Fault is the most prolific gold-bearing fault in the emerging Central Gold District and trends for a minimum of twenty kilometres at Gold Anchor. The fault hosts gold resources and high-grade drill intersections on trend to the northeast of our property. Our plan is to be drill-ready this fall to evaluate the Lane Pond Gold Target with an inaugural drill program.”

Comments