-01.png)

CHF WEEKLY ROUND-UP: July 21-25, 2025

- John A

- Jul 25, 2025

- 6 min read

World shares rose this week, buoyed by optimism that more trade deals will follow the U.S.-Japan tariff agreement announced on Wednesday. Investors are welcoming of recent tariff deals and expect more before the August 1 deadline set by President Trump. The European Union and the U.S. appear headed toward a trade deal similar to the agreement struck with Japan, that would include a broad tariff of 15% on EU goods imported into the U.S., including autos, and mirroring the framework agreement with Japan. European leaders also looked forward to substantial progress in cutting the bloc’s large trade deficit with China at a summit with President Xi Jinping in Beijing. Trump also announced trade agreements with the Philippines and Indonesia this week. The U.S. and China agreed in May and June to substantially lower their respective trade tariffs on each other and signed a framework trade agreement. Both sides are now attempting to seal a bigger deal, as the U.S. still maintains tariffs of between 30% to 50% on Chinese goods.

Canadian Prime Minister Mark Carney met with Provincial first ministers on Tuesday to update the premiers on trade talks with the U.S. Still, he made no guarantees a deal will be in place by the August 1 deadline, on which tariffs of 35% will be applied on some Canadian goods that aren’t covered under the existing North American free trade agreement. Carney has lowered expectations about reaching a trade agreement in the available time, saying “Canada will not accept a bad deal” and that the federal government is pursuing an agreement that will be in the best interest of Canadians. However, if having “elbows-up” and “NO DEAL” means facing higher tariffs than Japan, the EU, and other countries, then that is not in Canadians’ best interest, and a serious blow to confidence in the country. Canada’s per capita GDP growth has lagged well behind the OECD average in every year between 2015 and 2024, according to World Bank data. In May, non-resident investors reduced their exposure to Canadian shares by $11.4 billion. Canadian investors bought $11.5 billion of foreign shares in May, including sizable acquisitions of U.S. shares. Nevertheless, the TSX has actually done better than the S&P 500, so far this year, up roughly 11% year-to-date, while the S&P 500 was up about 8%. The TSX managed to record another all-time high this week. Still, shares are tentative at the end of the week as investors continue to be concerned about the outlook for U.S. trade policy during the coming quarterly earnings season. The Venture exchange index continued its uptrend and reached its highest since March 2021 this week, and is up 40% in the last 12 months (35% YTD).

The S&P 500 and Nasdaq edged up to record high closes on Wednesday and are pointed higher this morning for a fifth consecutive day of gains, looking to continue the rally through the summer. Asian and European stocks were mostly weaker overnight. Investors have been welcoming of President Trump's recent tariff deals and expect to see more before the August 1 deadline, on which the US will impose reciprocal tariffs on goods imported to the U.S from trading partners.

Federal Reserve Chair Jerome Powell will remain in office until the end of his term, but administration officials will undoubtedly continue to beat up on the Fed, especially if they decide not to lower rates next week. A strong June jobs report, which added 147,000 non-farm payrolls and the unemployment rate dropped to 4.1%, has significantly reduced expectations for a July cut. Fed Chair Powell and other Fed policymakers have emphasized a cautious, data-dependent approach, citing persistent inflation above the 2% target and uncertainties from tariffs. Most market participants and analysts now expect the Fed to hold rates steady at 4.25%-4.50%, with a rate cut in September being more likely. The latest batch of weaker-than-expected inflation reports may persuade Chair Powell to openly signal they are leaning toward lowering the federal funds rate at the September 16-17, 2025, meeting. On Thursday, the European Central Bank left interest rates unchanged at 3.75%, as was widely expected. There’s little expectation that the Bank of Canada (BoC) will make any changes to interest rates in the next rate announcement, set for Wednesday, July 30, 2025. The interest rate has remained at 2.75 per cent since March 2025. BoC Governor Macklem has stated that the bank will be more cautious with its interest rate changes in the coming months, but some economists suggest that two additional rate cuts could occur this year.

The precious metals continue to face selling pressure as investors take profits following a surge in Gold to above USD$3,430/oz earlier in the week. Spot gold last traded today at USD$3,343/oz, sitting at its support level. Central banks and sovereign wealth funds, particularly from Asia and the Middle East, looking to hedge risks and preserve value, have continued buying in the first half of the year. Sustained buying by these players serves as a powerful floor under gold prices, reinforcing the metal’s strategic appeal amid macroeconomic uncertainty. Official sector demand is expected to keep prices supported above USD$3,300/oz. Gold and precious metals have been a bright spot for Canada this year, helping the TSX Composite Index outperform the broader market.

M&A activity in the gold sector continues with Augusta Gold announcing a definitive merger agreement with AngloGold Ashanti, where AngloGold will acquire all of Augusta's outstanding shares for CAD$1.70 per share in a cash transaction that values Augusta at CAD$197 million.

Even with silver approaching USD$40/oz, down to USD$38.60/oz this morning, it is still historically undervalued relative to gold. Venture-listed silver-based issuers are seeing a lot of attention, as are silver-backed ETFs. Platinum and palladium both made fresh highs this week.

Copper prices are holding steady near USD$5.75/lb today, with little other movement in base and industrial metals observed. On the supply side, Teck Resources will invest CAD$2.4 billion in Canada’s largest copper mine, extending the life of the Highland Valley copper mine in southern British Columbia that produced 102,000 tons of copper last year into the mid-2040s.

Battery, critical and electric materials continue to struggle. Presently, Chinese companies control roughly 25% of the world’s lithium mining capacity, and U.S. officials have warned that China is now producing “much more lithium than the world needs” and using that overcapacity to drive prices down until rivals “disappear”. Major Chinese battery makers own or have stakes in overseas mines, often shipping ore to their own refineries. China sources ore from abroad, refines it domestically, and locks it into its own EV supply chains, largely ignoring global price signals. Chinese producers already make about two-thirds of global battery-grade lithium chemicals. Beijing-linked firms now dominate the entire production chain, from mining to battery manufacturing. Exposure to this sector should be targeted at participants with the best projects and economic advantages, rather than broad investment.

We are pleased to present our round-up of client news released between July 21 and 25, 2025.

Mining

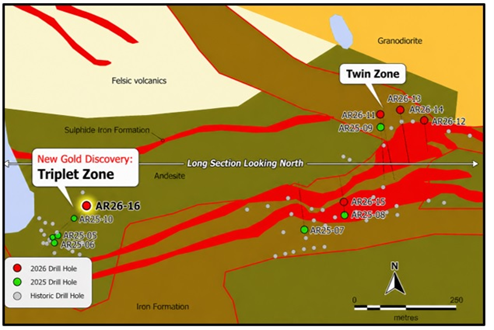

On July 24, 2025, Sokoman Minerals Corp. (TSXV: SIC) (OTCQB: SICNF) provided the following updates on its core properties in central/north-central Newfoundland: Moosehead, Crippleback and Fleur de Lys.

Timothy Froude, P.Geo., President and CEO, states, “A delay in the bulk sampling program at Moosehead has opened a window of opportunity to implement recommendations stemming from Dr. Coller’s structural report on the property. In addition to a robust shallow drilling program, Dr. Coller and Exploration Manager Ryan Newman have proposed three “deep holes,” each 1,000 m in length, reaching a vertical depth of 800 m. These will test for extensions of the known gold zones, intersect untested structures and guide further deep drilling. Drilling is scheduled to commence later this year, contingent upon receipt of the necessary permits.”

Fintech

On July 23, 2025, Tenet Fintech Group Inc. (CSE: PKK) (OTCQB: PKKFF) announced that the completion of the audit of the Company's year-end 2024 financial statements would be further delayed to align with the annual tax audit of the Company's Chinese subsidiaries. The subsidiaries' tax audit is an annual requirement for Tenet's Chinese operating entities. It is typically conducted alongside the audit of the Company's year-end financial statements, as both audits rely on similar financial information. This year, however, Tenet was unable to synchronize the two audits because of the delay in the start of the audit of its Canadian operations, resulting in additional delays in filing the Financial Statements. Tenet has revised the timeline for filing the Financial Statements to August 2025, with a precise filing date to be communicated by the end of this month.

Comments